Paying off debt can be a daunting task, especially when you don’t know where to start. It’s important to understand your options so you can make the best decision for your financial situation.

When it comes to paying off debt, there are two popular strategies and you may have already heard of them both: the Debt Snowball Method and the Debt Avalanche Method.

While both have their pros and cons, it’s important to know which one is right for you in order to effectively pay off debt. In this blog post, I’ll be taking a deeper look at both methods to help determine which is the better way to help you pay off debt!

“The average American debt (per U.S. adult) is $58,604 and 77% of American households have at least some type of debt.”

Ramsey solutions

Table of Contents

What is the Debt Snowball Method?

The Debt Snowball Method, made famous by personal finance guru Dave Ramsey, is a strategy for paying off debts that involves tackling your smallest debt first and gradually working up to the larger ones. The idea is to get rid of one debt at a time, beginning with the smallest one.

This approach can help provide you with a sense of accomplishment and motivation as you see each debt paid off.

When using the Debt Snowball Method, you list all your debts (not including a mortgage), from smallest to largest, ignoring interest rates. You make the minimum payments on all your debts except for the smallest one. Then, you take all the money you have available (after setting aside money for emergency savings and paying your minimum monthly expenses) and apply it to the smallest debt until it’s paid off.

TIP: The debt snowball method is typically applied to credit cards, though it also can be used to pay off student loans, auto loans, personal loans, and other lines of credit.

INVESTOPEDIA.COM

Once that debt is paid in full, you move on to the next smallest debt, applying the same method. You’ll have a larger amount to put towards the second debt, because you won’t have the first debt’s minimum payment and that amount can be applied to the next debt… which creates a snowball effect. Once the second debt is paid off, you’ll have a larger amount to put toward the third debt. Each time the amount gets larger and larger.

As you pay off each debt, you’ll start to see your overall debt decrease, providing motivation to keep going until all of your debts are paid in full.

The Debt Snowball Method is a popular option because it can provide psychological benefits, making you feel like you’re making real progress on your debt, which can be motivating. The Debt Snowball Method also emphasizes making changes in your spending habits, which can help create long-term financial success.

What is the Debt Avalanche Method?

The debt avalanche method sometimes referred to as the “debt stacking” approach, is a debt repayment strategy that prioritizes paying off high-interest debt first.

The idea behind the debt avalanche method is simple: by focusing on paying off the debt with the highest interest rate first, you can save money over the long run by reducing the total amount of interest you pay.

To begin, list all your debts from highest to lowest interest rate, regardless of the amount. Then, make the minimum payments on all other debts while dedicating as much money as possible to paying off the highest interest-rate debt. Once that debt is paid off, roll the payments over to the next highest interest-rate debt and continue until all your debts are gone.

For those who prefer to be very organized and want to pay off their debts in the most cost-effective way, the debt avalanche method may be the best option. By carefully tracking each debt and its interest rate, this method can help you save time and money. Additionally, this approach can also be a powerful motivator, as you can watch your progress and celebrate every time you pay off a high-interest debt.

However, it can become easier to lose steam — depending on the balance — the highest-interest debt may take longer to pay off. Meaning you’ll have to be self-motivated to continue paying it down even when not seeing the paid-off debt right away.

IMPORTANT: To be successful, before embarking on the debt avalanche program, you should have enough money in the bank for both living expenses and emergencies.

INVESTOPEDIA.COM

So, which method is right for me?

When deciding which debt repayment method is best for you, it’s important to consider the pros and cons of both the Debt Snowball and Debt Avalanche methods.

The Debt Snowball method entails paying off smaller debt balances first, regardless of interest rate. This can be an effective way to motivate you, as you can take pride in seeing the number of debt balances decrease quickly. The downside to this approach is that you may end up paying more in interest, since higher-interest debts are not being paid off first.

The Debt Avalanche method requires you to pay off the debts with the highest interest rates first, regardless of the balance. This is generally seen as the most cost-effective option, as it will save you the most money in interest over time. The downside is that it can take longer to make a dent in your total debt balance or the number of debt accounts due to the higher interest rates.

Which method is best for you ultimately depends on your goals and financial situation… as well as the way your mind operates. If you need a sense of accomplishment from seeing progress quickly, the Debt Snowball might be the better choice. However, if your main priority is saving money, the Debt Avalanche might be more appealing. In any case, the important thing is to create a plan and stick to it.

What method are we paying off debt with?

We’ve used a mix of both!

We started out with The Debt Snowball, because that’s what we knew to do, and it worked well for us. In fact, over the past couple of years, we paid down over _______________

At the end of the day, it’s important to do what’s best for you and your financial situation. You may want to consider using a debt calculator or talking to a financial advisor to help you decide which method is right for you. No matter which method you choose, the key is to stay consistent and make sure you’re making payments on all your debts each month.

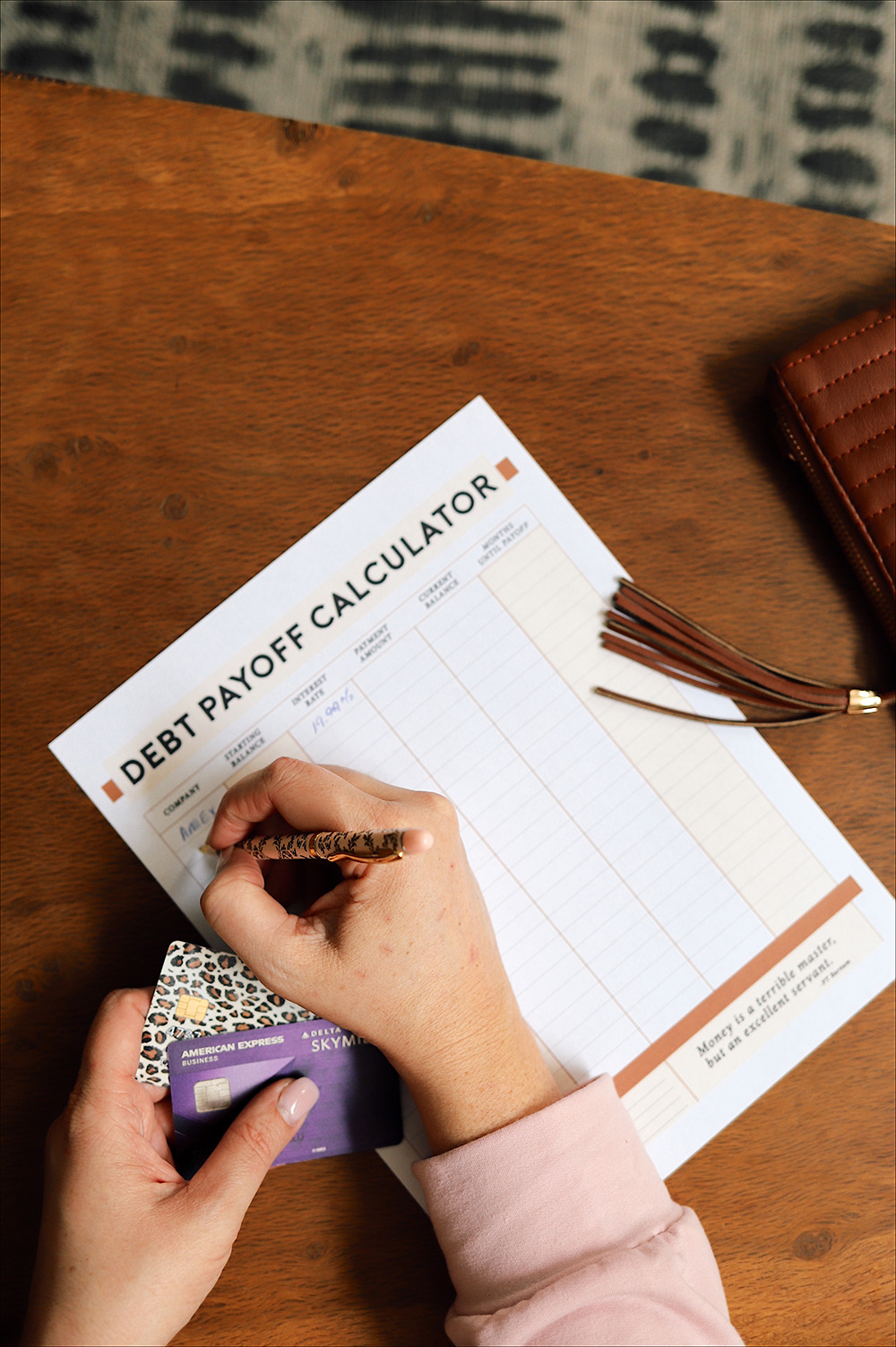

Free Download to Calculate Debt Payoff!

When it comes to debt payoff, having a plan is the key. Whether you are using the debt snowball or avalanche method, having a plan of attack is essential. That’s why we created a Debt Payoff Calculator Sheet that you can use to help figure out which method works best for you and your situation.

This calculator sheet allows you to list out all of your debts and input the minimum payment amount each month, as well as the interest rate of each debt. From there, you can choose between either the debt snowball or debt avalanche method.

Print and reprint as many times as you need, and rearrange and fill out the sheet as it best suits you… and then CROSS OFF THOSE DEBTS as you pay them off. That’s the best part!

We have been using this calculator sheet for YEARS now, and it has been a great way to get all of our debts in front of us at a glance. We highly recommend downloading it to get started, no matter which method works best for you.

Download the Free Debt Payoff Calculator Sheet Now and Get Started on Creating Your Debt-Free Future!

{kind=link}

Lat says

This is such a helpful breakdown of the Debt Snowball and Debt Avalanche methods! Choosing the right approach can make a huge difference in staying motivated and effectively tackling debt. The free debt payoff calculator is a great bonus—thanks for making it easier to take that first step!